In order to create a comprehensive financial plan, there are many considerations that need to be taken into account. The key is to start with the end in mind and work backward from there.

That means knowing what you want your future self to look like before deciding how much time or money you should spend on different aspects of your life now.

Table of Contents

What is a financial plan?

A financial plan is a document that includes your financial goals, objectives, and the steps needed to take in order to reach them.

A financial planner may prepare this for you by getting answers to some key questions: What are the short-term and long-term needs of an individual or family? How much money can be spent each month, and from what sources? How much money will it take to reach financial goals or objectives over the short-term or long term?

This blog post will provide 8 tips for creating the perfect financial plan!

1. Identify your financial goals

Before you get started, you need to determine your goals and objectives. Everyone has financial goals, whether they have a financial plan or not. Figuring out what those are is the first step to creating one for yourself.

Financial goals could be to save for retirement, pay off the mortgage early, buy a car or simply make sure you have enough money in your savings account.

After identifying financial goals and objectives, it’s time to start building a budget that will help guide these goals.

2. Create a budget and stick to it

A financial plan is not complete without a budget. This will help you decide what to invest your money in, as well as how much of each spending category (i.e., groceries vs gas) you should spend every month so that it can be balanced out and accounted for properly.

Make sure you write a budget that is going to be sustainable for the long term. You may need to make adjustments every now and then, but your financial stability should be able to withstand any unexpected changes in expenses.

Don’t confuse this with just spending less money; it’s about being more intentional with where you spend your money on things.

3. Pay off any debts you have as soon as possible

The sooner you can pay off any debt that has accumulated, the better chances you have of creating a life plan that will be sustainable in the long run. Consider allocating some money every month to pay off your debts if you can.

If you’re not sure how much debt you have, get detailed information from each of your financial institutions. You may be surprised by the number that comes up and then it’s worth taking a bit more time to strategize about which ones should be paid off first.

It will also help you to see how much of your monthly income you have left after paying off debt. This is a great time to figure out what else you want or need in the future that may not be possible right now with this amount of money.

4. Track your spending

It’s common for people to underestimate how much they spend on things like eating out, going out, and shopping.

If you are able to track your spending over the course of a month or year, it should give you an idea about what expenses have been weighing down your budget.

An easy way to start is by creating a budget from your current paystubs and tracking spending on weekly basis.

Categorize each expense into different categories like rent, food, utilities, etc., this will give you an idea of where the majority of your money is going right now.

When comparing your budget to your spending, it might be necessary to make some changes.

For example, if you’ve been spending $100 a week on food and want to cut back that number, try switching up what types of groceries or restaurants you visit each month.

This will allow for more financial flexibility in the future.

5. Set up an emergency fund

Establish an emergency fund for the worst-case scenario. Ideally, this should be three to six months’ worth of living expenses set aside in a savings account that you can access without penalty if your income is cut off.

If it’s too difficult to save enough money or if you don’t have any cash reserves, try putting away any extra you have into a high-yield savings account. It’s better to have some money no matter how small the amount than none at all.

The emergency fund should be planned to cover any financial needs that may occur in the future, such as a sudden medical bill (or one for an uninsured family member), car repairs, and home maintenance costs. For some people with irregular incomes like freelancers, this is even more important.

Some financial planners recommend that families have an emergency fund equal to three times the annual family income, but even if you just save a few thousand dollars in cash or in high-interest savings accounts, it can still make a big difference.

6. Contribute to retirement savings

If you are looking to create the perfect financial plan, then there is one step that must be taken. Contribute to your retirement savings.

If this is not done first, it will likely never happen at all. It’s hard enough setting aside money for a rainy day or paying off debt if you have anything left over after living expenses.

It doesn’t matter what your financial situation is, the sooner you start saving for retirement, the better off you will be later in life.

If you are earning a paycheck, then there should be something set aside automatically from every paycheck to go into an employer-sponsored 401(k) or equivalent plan on your behalf. If this is not done, then you are missing out on a potentially huge nest egg.

Many people underestimate how important a retirement account is. Consistently saving at least 15% of your paycheck can yield huge returns in the long term.

As a matter of fact, Ramsey Solutions conducted the largest survey of millionaires ever (10,000 participants) and the results were astonishing. Eight out ten millionaires became a millionaire just by investing in their company’s 401(k) plan.

If your employer does not offer this you can open a Roth IRA on your own at your bank. There are many forms of these accounts that can be set up and they will help you build wealth at your own pace.

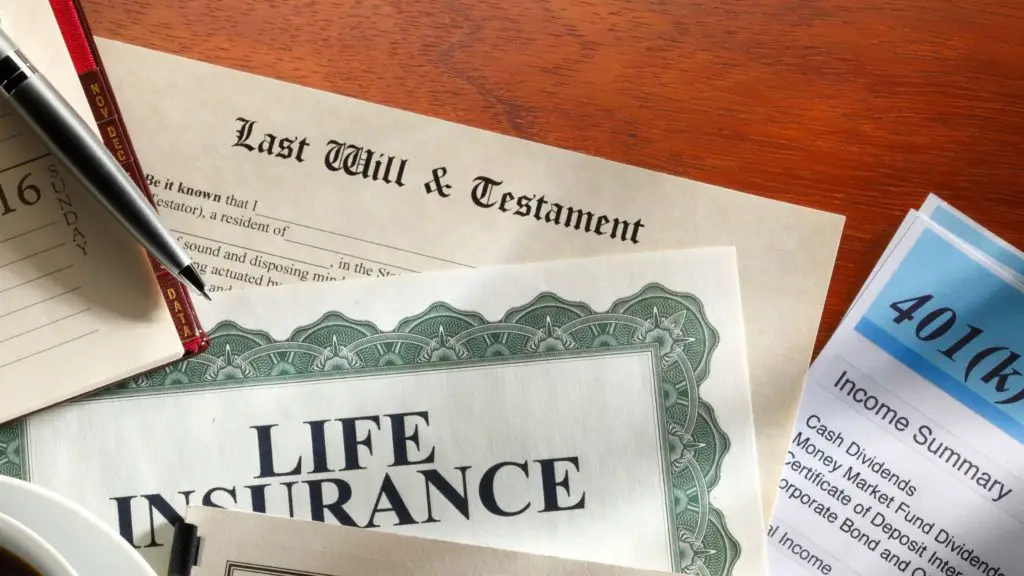

7. Consider investing in life insurance

Life insurance is a type of financial product that pays out in the event of death, typically to help with surviving family members.

It can also provide for final expenses and allow you to keep making payments on your mortgage or loan obligations if these are taken out as part of the policy (known as “life cover”).

According to life insurance brokers, taking out a life insurance policy is as important for single people who have sufficient assets to cover final expenses, as it is for those with dependents.

You will need to determine how much of an income you would like your beneficiaries to receive from the policy, and what the maximum amount of benefits should be.

The decision to take out life insurance is a personal one, but it can help relieve financial stress on your loved ones if you were to die unexpectedly.

Insurance brokers often say that people who have dependents should consider buying life insurance because if they were to die, their dependents might be unable to meet financial obligations such as mortgage payments or college tuition.

It may also provide for future financial goals such as retirement or education expenses.

8. Create an estate plan

An estate plan (or will) is an essential part of financial security, but many people don’t know how to create one. There are a few key steps that you need to take in order for the process to go smoothly:

- determine who should be your executor and trustees;

- decide which assets you want to be included in your will

- determine how you want to distribute your estate;

- make sure that any agreements you have made with other people are included.

To avoid common mistakes, it’s a good idea to consult an attorney or financial planner before the process begins. In addition, there are many online tools and services available for assistance in creating wills all of which are accessible through the internet.

The perfect financial plan is the one that takes into account your unique needs and goals.

It’s not easy to create a perfect financial plan, but the tips in this blog post should help you get started. To recap, we’ve covered eight ways that you can start planning for your next steps and future goals.

You may want to brainstorm now what type of things are important to you in order of importance so that when it comes time for decision making, you have your priorities straightened out.

This will include thinking about how much money do I need? How will I spend my money? What is my goal with these finances?

If there was one tip from my list that resonated most with you, which would it be or why did it resonate more than others? I hope this blog helped answer some questions on creating an effective financial plan.